An opinion from a former State Insurance Regulator

The promise of life insurance is simple: protection when it matters most. Policyholders pay premiums over decades with the expectation that, if something goes wrong, their families will be financially secure. As a former State Insurance Commissioner and Vice Chair of the NAIC Life Insurance and Annuities Committee, I approached that promise from the consumer’s side; ensuring that coverage performs as expected when tested.

But there is a gap between expectation and reality that deserves more attention, particularly in today’s geopolitical environment.

A Lesson from Conflict

During my time as a regulator, issues surrounding war exclusions were not theoretical. They arose in real time during periods of heightened conflict, including the Hamas takeover of Gaza and the subsequent Israeli military operation known as Operation Cast Lead. In those moments, questions surfaced about how life insurance policies would respond if U.S. citizens were killed abroad.

The answer, even then, was not always straightforward.

Consumers understandably assume that life insurance follows them wherever they go. In practice, coverage can narrow significantly depending on where you are, what is happening in that region, and how your policy defines risk.

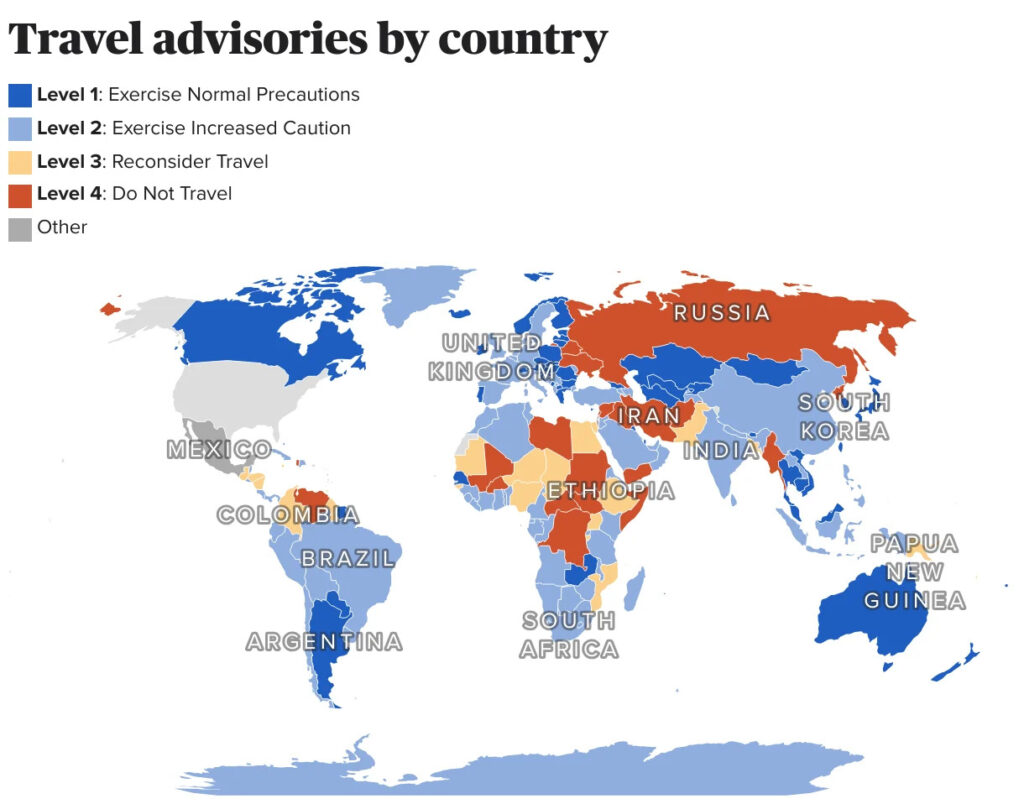

The Role of the State Department: A Quiet Underwriting Tool

Life insurers do not operate in a vacuum. One of the most important, yet often overlooked, inputs into underwriting and claims decisions is the guidance issued by the U.S. Department of State.

The State Department assigns four travel advisory levels:

· Level 1 – Exercise Normal Precautions

· Level 2 – Exercise Increased Caution

· Level 3 – Reconsider Travel

· Level 4 – Do Not Travel

These are not merely travel suggestions. In many cases, they serve as de facto risk signals for insurers; informing underwriting decisions, shaping exclusions, and influencing how claims are evaluated. As an insurance regulator we turned to these threat levels to help guide life insurance companies on underwriting the risk on our citizens abroad.

Review your policy and watch for any changes to your policy. With the existing Middle East conflict it is safe to assume that the insurance companies are reviewing their language closely.

A Timely Reminder: Worldwide Caution

As of Sunday, March 22, 2026, the State Department issued a “Worldwide Caution” security alert, advising Americans, particularly in the Middle East, to exercise increased vigilance.

Key elements include:

· Elevated risks to U.S. citizens and interests abroad

· Potential targeting of diplomatic facilities

· Possible travel disruptions, including airspace closures

· Increased threat activity from groups aligned with geopolitical actors

The guidance is clear: monitor embassy alerts, review destination-specific advisories, and enroll in traveler notification systems.

From an insurance perspective, the message should be equally clear.

Why This Matters for Your Life Insurance

Most life insurance policies contain war or conflict exclusions, but they are not uniform. They vary from company to company. Some apply only if death is directly caused by war. Others are broader, capturing deaths that occur in connection with conflict-related events.

The practical issue is this: When geopolitical risk rises, the line between “covered” and “excluded” can become blurred.

Consider:

· A civilian traveling in a region that rapidly escalates into conflict

· A targeted attack with unclear classification; Terrorism or Act of War

· A death occurring amid unrest but not directly tied to combat

These are precisely the kinds of cases that lead to disputes between insurers and beneficiaries.

The Consumer Perspective: Trust vs. Technicality

As regulators, our role was to represent the consumer, the individual who purchased a policy in good faith (often years earlier) without anticipating the complexity of geopolitical risk.

From that vantage point, a consistent concern emerged: policyholders rarely understand how exclusions operate until it is too late.

The technical language: “Act of War,” “Undeclared Conflict,” “Indirect Cusation” may be clear to lawyers and actuaries. It is not clear to most families.

A Practical Recommendation: Check Before You Travel

This is not an argument against travel. It is an argument for informed travel.

Before traveling internationally, particularly to regions with elevated risk, policyholders should:

· Review their life insurance policy Focus specifically on war, terrorism, and travel-related exclusions

· Check the State Department advisory level for the destination

· Disclose travel plans if required Failure to disclose can create separate grounds for denial

· Consider supplemental coverage if exposure is elevated

· Monitor real-time developments Conditions can change faster than policyholders expect

A Broader Reality

Life insurers are not indifferent to consumer outcomes. But they are managing systemic risk; a risk that becomes highly correlated during conflict. War exclusions are, in part, a reflection of that reality.

At the same time, consumers reasonably expect that the protection they purchased will be there when needed.

Bridging that gap requires greater awareness.

Final Thought

Life insurance is designed to provide certainty in uncertain times. Yet in a world where conflict is less formally declared and more globally dispersed, that certainty can erode at the margins.

Before you travel, check not just your destination, but your coverage.

Sean Dilweg served as the Wisconsin Insurance Commissioner from 2007 to 2011. As Vice-Chair of the NAIC’s Life and Annuities Committee he worked with fellow regulators on life insurance regulation nationally during the Great Recession. He now serves an expert witness regarding insurance regulation, financial and credit policy having been retained in various states and federal court.

Related Posts

2nd Lien 2 Step

Freddie Mac’s new pilot program seeks to purchase closed-end second mortgages, a move that generated..

How to Address Growing Wildfire Threats: Natural Catastrophe Insurance Interstate Compact

Republicans have expressed their concerns over the SEC overreach on Environmental Social and Governance..

Banks Profitability Stable Leading into Powell’s Jackson Hole Speech

As the dust settles on Q2 bank earnings calls, a key indicator of financial health…

Bowman overplaying her hand vs Michael Barr

Michelle Bowman, the Fed governor in charge of community bank issues, and a Trump appointee,…